On a warm day in September 2009, Jason Hargett, a 35-year-old restaurant manager and father of 4, stepped up to the tee at Red Ledges golf resort in Heber City, Utah.

It was the end of a charity tournament and a big prize was on the line: Anyone who sunk a hole-in-one would win $1m.

Hargett took a swing.

The ball careened 150 yards through the air, plopped onto the green, and slowly rolled back into the hole. Cheers erupted from the small crowd as Hargett sprinted down the fairway in disbelief.

But one entity wasn’t celebrating: the insurance firm that had been hired by the organizers.

***

If you’ve ever watched a golf tournament or charity event, you’ve probably seen some kind of prize (a cash payout, a flashy car, a vacation package) for acing a specified hole.

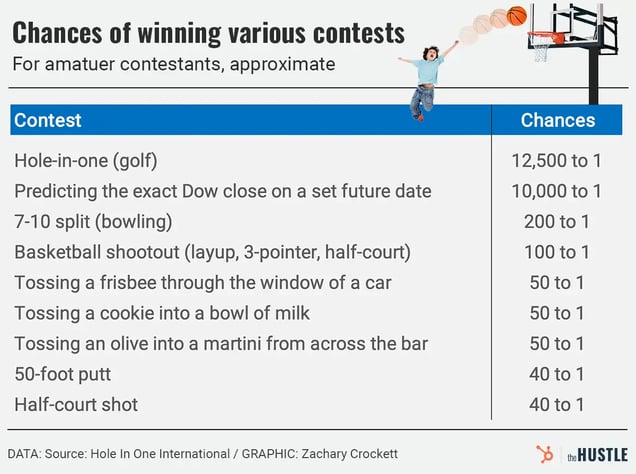

The chances of this happening for an amateur golfer are minuscule (~1 in 12.5k). But most organizers can’t risk getting stuck with the bill.

Instead, they turn to hole-in-one insurance firms that assume the risk for a small fee.

A brief history of ‘unlucky’ golfers

The hole-in-one insurance business dates back nearly 100 years — but it was originally intended for a different purpose.

In many golf circles, it was (and still is) customary for the lucky golfer to buy drinks for everyone in the clubhouse after landing a hole-in-one. This often resulted in prohibitively expensive bar tabs.

And an industry sprouted up to protect these golfers.

Tiger Woods serves drinks during the Johnnie Walker Classic in 2000 (David Cannon/ALLSPORT)

A newspaper archive analysis by The Hustle revealed that hole-in-one insurance firms sprouted up as early as 1933.

Under this model, golfers could pay a fee — say, $1.50 (about $35 today) — to cover a $25 (~$550) bar tab. And as one paper noted in 1937: “The way some of the boys have been bagging the dodos, it might not be a bad idea.”

Though the concept largely faded away in the US, it became a big business in Japan, where golfers who landed a hole-in-one were expected to throw parties “comparable to a small wedding,” including live music, food, drinks, and commemorative tree plantings.

By the 1990s, the hole-in-one insurance industry had a total market value of $220m. An estimated 30% of all Japanese golfers shelled out $50-$70/year to insure themselves against up to $3.5k in expenses.

Around the same time, golf tournaments began offering increasingly large prizes for holes-in-one as a way to drum up press.

And hole-in-one insurance began to make a comeback in the US — not for individual golfers, but for the event organizers putting up the money.

How hole-in-one insurance works

Mark Gilmartin runs Hole In One International, one of the oldest hole-in-one insurance companies in the US.

The idea first struck in 1991, when Gilmartin, then 29 and the proprietor of a golf club repair company, saw a burgeoning need for prize coverage at charity events.

Since 1991, his Reno-based firm has paid out ~$56m in insurance claims — including Jason Hargett’s $1m prize.

Mark Gilmartin (photo illustration: The Hustle)

Today’s hole-in-one-insurance landscape, Gilmartin says, is ripe with competition: More than 2 dozen companies specialize in the niche field, vying for Google search keywords and golf tournament dollars.

The process generally works like so:

- A golf tournament decides to give away a prize — say, a $60k Mercedes — to anyone who gets a hole-in-one at the event.

- They partner with a sponsor (in this example, a dealership) that offers the prize.

- The sponsor pays Hole In One International a relatively small fee ($200 to $1k+); if someone gets a hole-in-one, Gilmartin covers the cost of the prize.

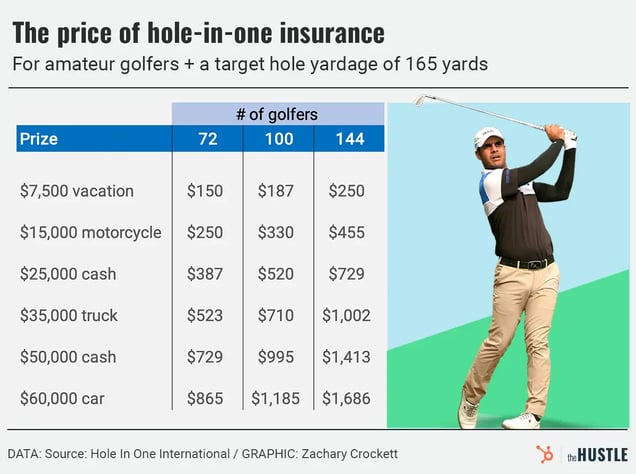

Gilmartin says the cost to insure against a hole-in-one is dependent on 3 factors:

- The number of golfers in the tournament

- The length (yardage) of the contest hole

- The cash value of the hole-in-one prize

Once a client provides this information, Gilmartin plugs it into an algorithm that computes the odds, factors in his risk and margins, and spits out a dollar amount per golfer.

A standard tournament with 100 golfers playing a 165-yard hole with a $10k prize sets an event back ~$235.

Zachary Crockett / The Hustle

Insurance firms operate on the premise that the odds of something happening are small enough to assume a repeated risk — and in Gilmartin’s case, this holds true.

The chances of someone getting a hole-in-one are fairly small:

- 1 in 12.5k for amateur golfers

- 1 in 3k for pro golfers

But ~450m rounds of golf are played every year. And because of the scale and popularity of the sport, the feat happens on a daily basis.

The National Hole-In-One Registry — the preeminent record-keeper of aces — estimates that 128k holes-in-one are achieved internationally every year by professionals and amateurs.

In other words, Gilmartin is no stranger to opening up his pockets.

What happens when someone wins?

Every year, Gilmartin says he insures ~15k events and pays out “hundreds and hundreds” of holes-in-one.

Most of those prizes are under $100k in value. But sometimes, he gets dinged up pretty bad.

In November 2021, for instance, 3 LPGA golfers got a hole-in-one in the same week, each winning a 2-year lease on a Lamborghini Huracán. The tournament’s sponsor, Morgan Auto Group, purchased hole-in-one insurance from Gilmartin, and the winning shots set him back ~$300k.

“Yeah, those women are pretty damn good,” he says. “That one still stings.”

Over the past 30 years, Gilmartin has also had to pay out at least 4 $1m prizes, which are typically awarded in annuities. Hargett, who landed that shot in Utah, got $25k/year for 40 years — a steep cost for Gilmartin, who charged a total of ~$1.1k to insure the 6 contestants at that event.

Pro golfer Austin Ernst with her Lamborghini Huracán after sinking a hole-in-one at the LPGA’s Pelican Women’s Championship in November 2021 (Austin Ernst / Instagram)

Before paying out a prize, Gilmartin requires a few proof-points:

- A sworn affidavit from an unbiased, non-participatory witness at the event.

- A “gentle investigation” of the hole-in-one’s legitimacy (verifying the tee position wasn’t changed, that the yardage was consistent with the contract, etc.).

Fraud does happen in the business.

In 1998, for instance, a man got a hole-in-one at an event and won a choice between a 1931 Cadillac or $40k in cash. But it turned out that the event organizer owed the winner a favor and had staged the whole thing. The organizer was convicted of fraud, and the prize was nullified.

But Gilmartin says prizes are rarely denied — and despite forking over $2-$4m in claims in any given year, he always ends up in the black.

“You’re going to get hit in this business, but hopefully it all comes out in the wash at the end of the year,” he says.

Cow poop, frisbee tosses, and half-court shots

Hole-in-one insurance is only one facet of a broader industry called prize indemnity insurance — the coverage of any promotional event in which a large prize is offered.

Gilmartin runs a second company, Odds On Promotions, that covers much weirder stuff than holes-in-one.

“If you can dream it, I’ll insure it,” he says.

Among the many events Gilmartin has insured prizes for:

- Half-court shots during halftime at basketball games

- Guessing the number of jelly beans in a jar

- Guessing the exact weight of a giant pumpkin

- Throwing a frisbee through the sunroof of a car

- Making a 7-10 split in bowling

- Rubber duck races

- Tossing a cookie into a bowl of milk

- Guessing the Dow Jones average on a set day in the future

- Tossing an olive into a martini glass from across a bar

Among the weirder things he’s insured? Cow patty bingo (video here).

“It’s big in the Midwest,” says Gilmartin. “You divide a big field into, say, 100 squares, give each one a number, then let a cow loose. If the cow poops on a preselected number, the person wins a prize.”

Zachary Crockett / The Hustle

All of these things are insurable, he says, because they fall into one of 3 categories of risk:

- Mathematical (like flipping a coin)

- Skill-based (a half-court shot)

- Odds-based (a sports team winning a game)

In most cases, Gilmartin can calculate the rough chances of something happening and use the data to compute his premiums.

But sometimes, he has to insure things for which data doesn’t exist. And in those cases, he re-creates the scenario himself.

If a sponsor wants contestants to throw a ping-pong ball through a hole in a watermelon, he’ll go outside with his employees and re-create it himself, recording the results.

“It keeps things exciting,” he says. “By insurance standards, at least.”