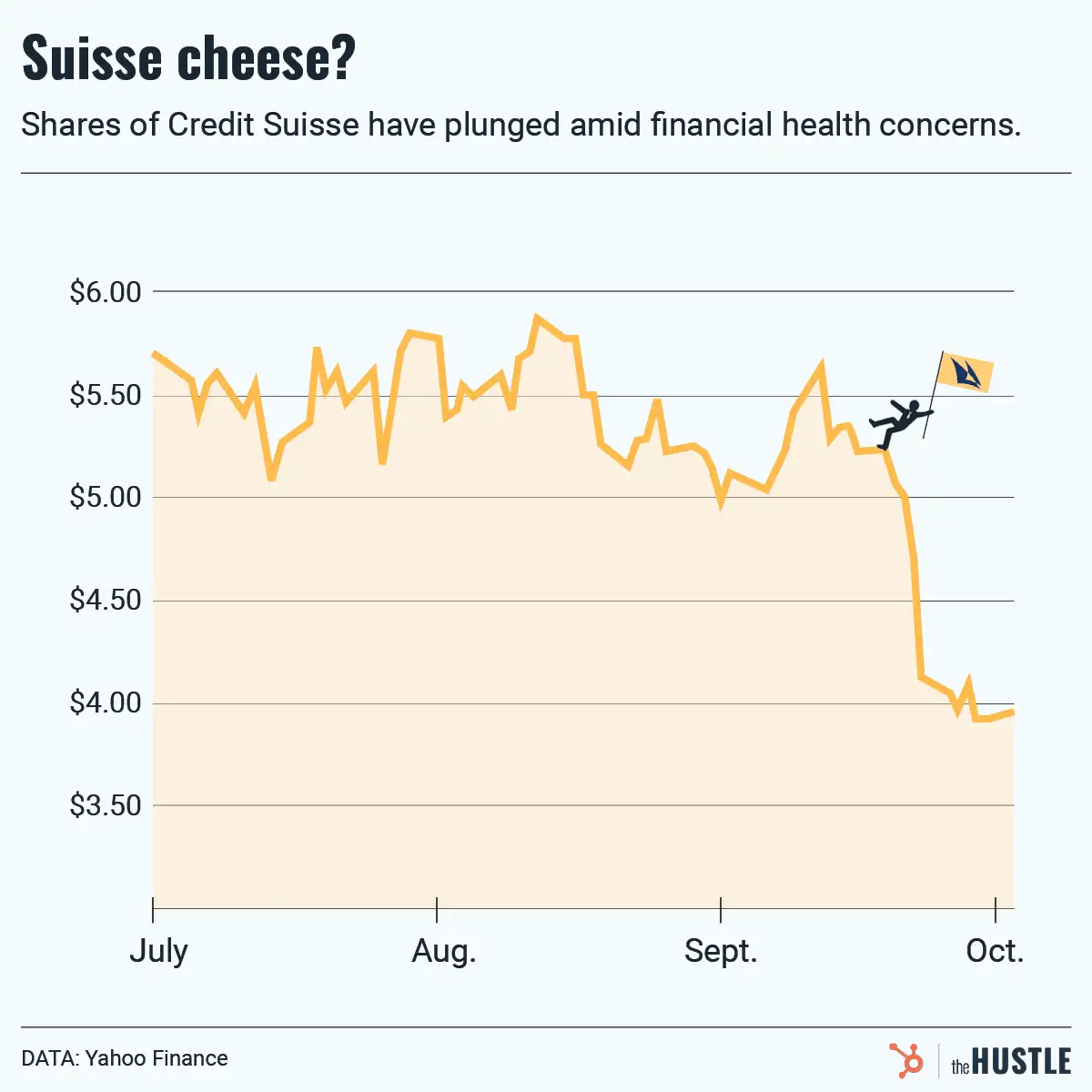

Over the past week, Wall Street has been picking through the implosion of a $10B fund called Archegos Capital Management.

A number of highly leveraged bets went sideways and the fund — run by industry vet Bill Hwang — went poof virtually overnight.

Per The Wall Street Journal, Hwang is purported to have personally lost $8B in 10 days while 2 global lenders (Credit Suisse, Nomura) are also reporting 10-figure losses.

While these numbers are big…

… the longer-term effects may send ripples through a much larger pile of money: The family office industry.

Family offices are privately held companies that manage assets for the superrich ($100m+ in investable assets) with the goal of preserving wealth over generations. The source of the funds can be from generational wealth or uber-successful entrepreneurs.

Per the Financial Times (FT), the industry’s numbers are staggering:

- 7k+ family offices globally (up ~40% between 2017 and 2019)

- ~$6T in assets under management across all the offices (nearly 2x the hedge fund industry)

- $1.6B is the average family office holding

Here’s the kicker: the industry is very lightly regulated

While hedge funds, endowments, and pensions are accountable to outside money, family offices are able to stay a secretive affair.

Dan Berkovitz — a commissioner of the Commodity Futures Trading Commission (CFTC) — believes the current disclosure requirements are totally insufficient as reported by FT.

“The information required would fit on a Post-it note,” he said in a statement regarding Archegos. “And… the annual cost of the filing [is] merely $28.50.”

What will happen next?

While many family offices employ boring financial strategies to preserve wealth, Archegos — which had a peak portfolio value of $100B+ boosted by bank leverage — shows the risk.

Even though Hwang admitted to securities fraud in 2012 (and paid a $44m fine), leading investment banks were happy to have his business.

In the aftermath of the real estate crisis, the 2010 Dodd-Frank Act tightened financial regulation. Post-Archegos, the industry may see new rules for family offices, banking services, and the specific financial product used in Hwang’s trades (called total return swaps).

All of this seems totally reasonable…